tax benefit rule calculation

Most countries define maximum amortisation rates or minimum number of years in which the amortisation of intangible assets can be deducted if at all. Upon the enforcement of the original rule in 2019 a taxpayer could claim only Rs3000 Rs600005 in his GSTR-3B in any tax period up to 31st December 2021.

Average Tax Rate Definition Taxedu Tax Foundation

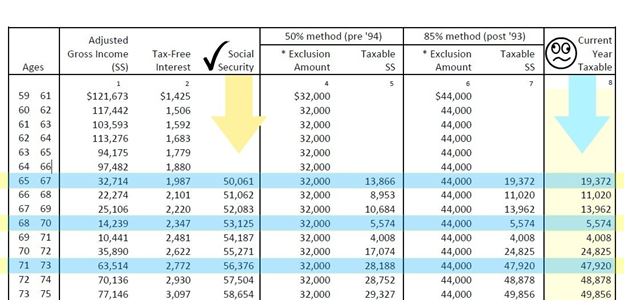

For clients with provisional income over 44000 joint A The portion of income between 32000 and 44000 is taxed according to the pre-93 rules at 50 amounting to 6000 of taxable social security.

. A tax benefit is an allowable deduction on a tax return intended to reduce a taxpayers burden while typically supporting certain types of commercial activity. Some tax benefits can show up directly on your paycheck whereas others have to be claimed on your tax return. If using the cents-per-mile rule to value the benefit for the employee you multiply the number of miles the employee uses the vehicle for personal use by the IRS standard mileage rate.

On Schedule A they listed real estate taxes of 7000 and state income taxes of 7000. 375 6 years 2250. Personal use is any use of the vehicle other than use in your trade or business.

A tax benefit allows. The rule is promulgated by the Internal Revenue Service. Individual Income Tax Return or Form 1040-SR US.

Of course if you were not able to itemize for 2012 none of your state tax refund is taxable for 2013. Visualizations from mobiles or small tablets may be incomplete. The calculation would be.

A tax benefit is a rule that allows you to pay less in taxes than you would without the benefit. You are given a 15-year bond with a face value of 1500 and it matures in six years. Significant tax savings can be obtained by understanding recognizing and.

There are exceptions to this principle which if exploited can reduce tax bills. But from 1st January 2022 they can claim nil provisional ITC. The following table displays the legal tax amortisation life times in years of the main types of intangible.

44000-32000 12000 x 5 6000. If the couple received a state tax refund of 500 in the current year the taxpayer will include. For 2022 the standard mileage rate is 585 cents per mile.

Calculation of net profit of self-employed earners. Tax benefits include tax credits tax deductions and tax deferrals. You would multiply that rate times the personal.

De minimis tax rule also applies to fringe benefits offered by employers. Jones recovers a 1000 loss that he had written off in his previous years tax return. Do not enter more than the amount deducted in the previous year.

The tax benefit rule requires Company XYZ to report the 100000 as income on its 2010 tax return and pay taxes on it. So the tax benefit you received from the 300 refund was only 225. The OECD Tax-Benefit web calculator enables users to compare how tax liabilities and benefit entitlements affect the incomes of working-age families across countries and over time.

Example with Calculation. The 1000 must be included in his current years reported gross income. The taxable refund for 2001 should be 25677 40000 14323.

The calculator has been optimized for laptops and tablets with a screen size bigger than 1024768. The rate for 2022 is 585 cents per mile. This amount must be included in the employees wages or reimbursed by the employee.

The tax benefit rule is a feature of the United States tax system. In other words they cannot claim. Its deductibility depends on the corporate income tax legislation of single countries.

B received no tax benefit from the overpayment of 750 in state income tax in 2018. 164 generally provides an itemized deduction for. Since the de minimis benefits offered are so small it will be.

When the couple paid the excess refund 400 to the state in the prior year it increased their itemized deduction on their federal return to 14000 from 13600. You can use the cents-per-mile rule if either of the following requirements is met. The entire amount recovered in the current year had given the taxpayer a tax benefit when originally paid.

Tax benefit rule calculation Monday May 16 2022 Edit. The steps are shown below. Compared to the new rule almost 70 exemptions have been removed in.

De Minimis Fringe Benefits. Its main principle is that if a taxpayer recovers a sum of money that should have been paid in the past they must pay tax upon it if it was not counted in their taxable earnings in a previous year. Example of the Tax Benefit Rule.

10000 250 1800 1500 2500 16050 total deductible payments for year 1 16050 22 3531 annual deduction for year 1 3531 12 29425 monthly tax benefit for year 1 For the short and long-term tax benefit the totals of each payment Interest MI UFMIP Property Tax Points for that period added. Income tax in 2018 Bs state and local tax deduction would have remained the same 10000 and Bs itemized deductions would have remained the same 15000. B The provisional income over 44000 joint is taxed according to the post-93 rules at 85.

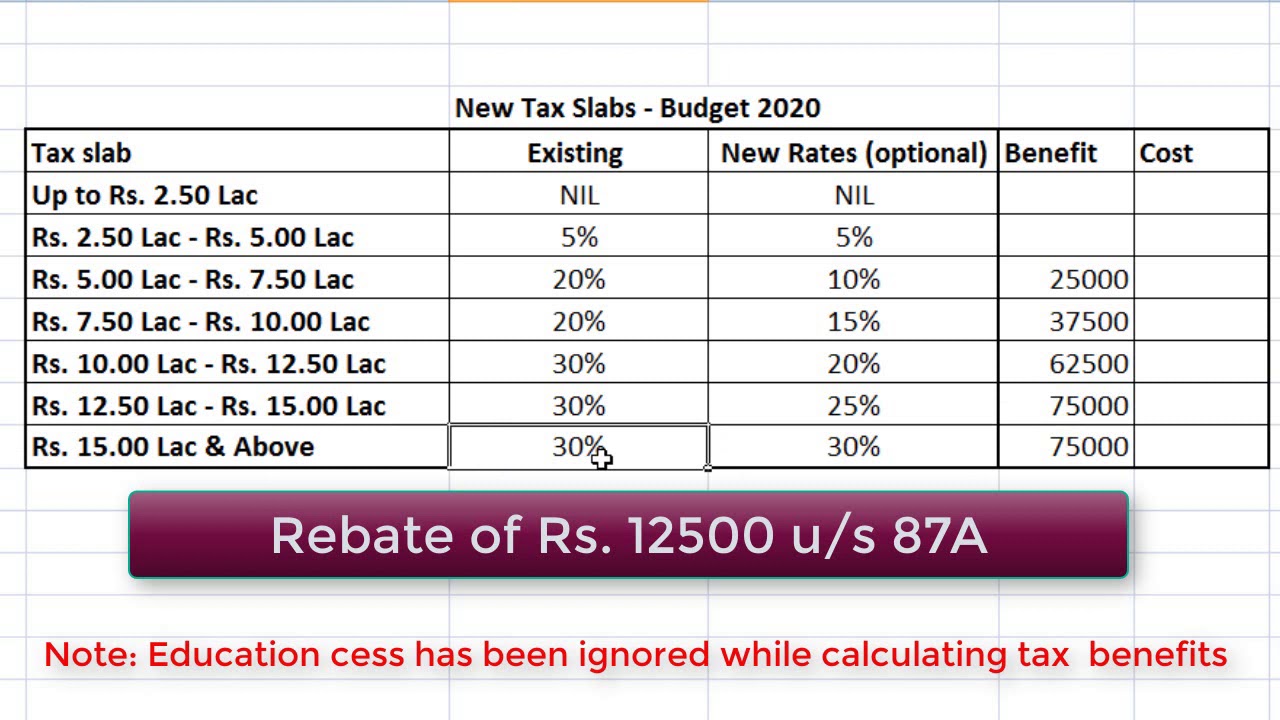

Personal use is for any mileage driven not for business purposes. New income tax slabs. Up to 25 lakh.

2019-11 issued on March 29 the IRS addressed how the long-standing tax benefit rule interacts with the new 10000 limit on deductions of state and local taxes to determine the portion of any state or local tax refund that must be included in income on the taxpayers federal income tax return. From 25 lakh- 5 lakh. The following examples provide an illustration of the mechanics of the tax benefit rule and how it should work with respect to the new law and the 10000 annual limitation.

A rule that if one receives a tax benefit from an item in a prior year because of a deduction such as for an uninsured casualty loss or a bad debt write-off and then recovers the money in a subsequent yearthe money must be counted as income in the subsequent year. Small Business Tax Guide. 2019-11 issued Friday the IRS addressed how the long-standing tax benefit rule interacts with the new 10000 limit on deductions of state and local taxes to determine the portion of any state or local tax refund that must be included on the taxpayers federal income tax return.

Joe and Denise Smith itemize deductions on their 2018 income tax return. Thus B is not required to include the 750 state income tax refund in Bs gross income in 2019. Therefore the taxpayer did not receive a tax benefit and 14323 of the 40000 is not subject to tax in 2001.

With the new income tax rule the tax calculation gets changed. Using tax software or working with a qualified tax professional can. State Local Tax SALT In Rev.

This article will try to learn about the new income tax its benefits and how the tax calculation differs.

Tax Benefits U S 80d How To Divide Health Insurance Premium To Claim Deduction For More Than 1 Year The Financial Express

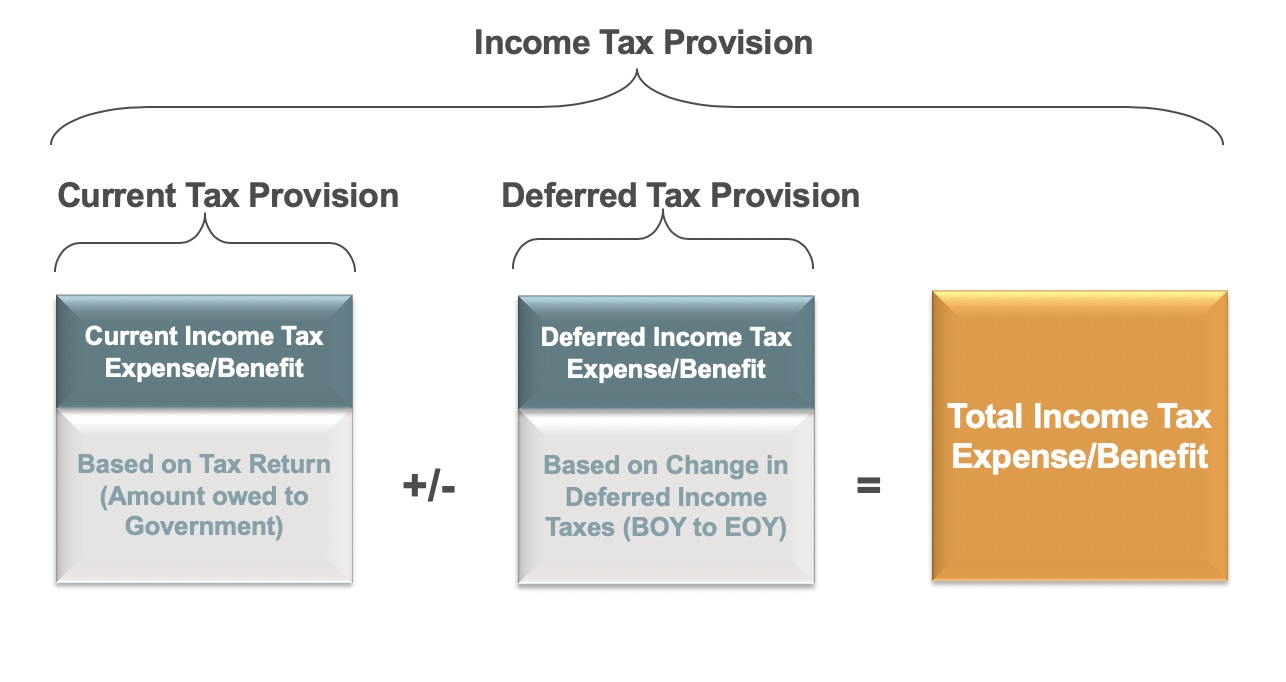

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

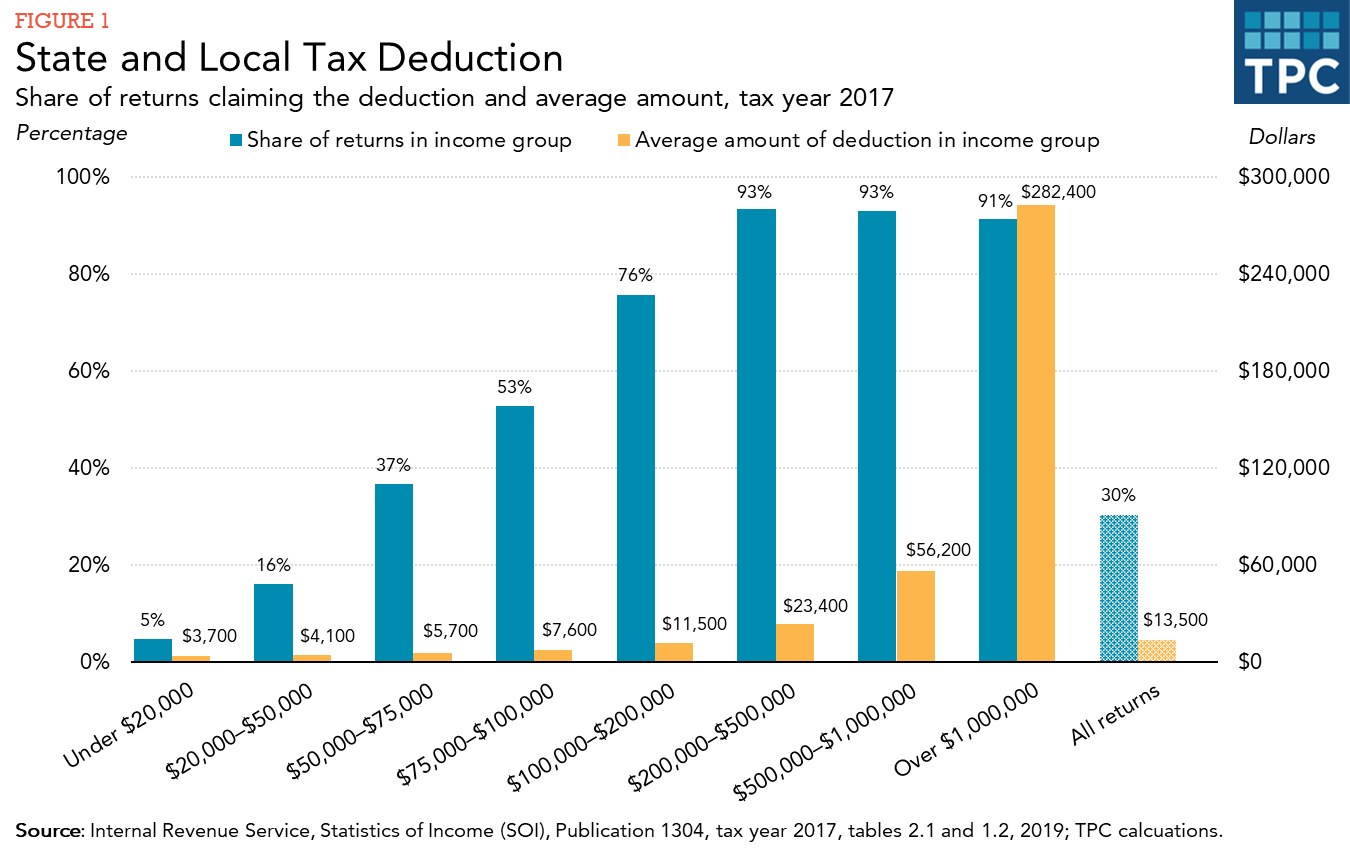

How Does The Deduction For State And Local Taxes Work Tax Policy Center

/dotdash_Final_Paying_Social_Security_v1_Taxes_on_Earnings_After_Full_Retirement_Age_Oct_2020-01-ec61e06a655442e9926572d10bb7d993.jpg)

Paying Social Security Taxes On Earnings After Full Retirement Age

Calculating Taxable Social Security Benefits Not As Easy As 0 50 85 Moneytree Software

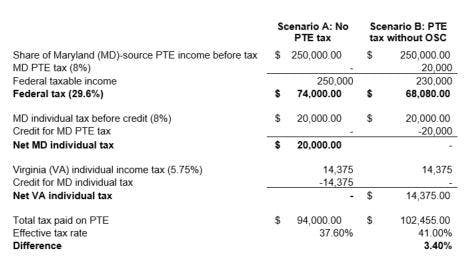

Pass Through Entity Tax 101 Baker Tilly

Budget 2020 New Income Tax Rates New Income Tax Slabs Income Tax Calculation 2020 21 Youtube

How To Calculate Income Tax Fy 2021 22 New Tax Slabs Rebate Income Tax Calculation 2021 22 Youtube

Tax Withholding For Pensions And Social Security Sensible Money

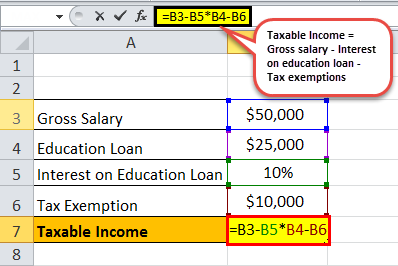

How Is Taxable Income Calculated

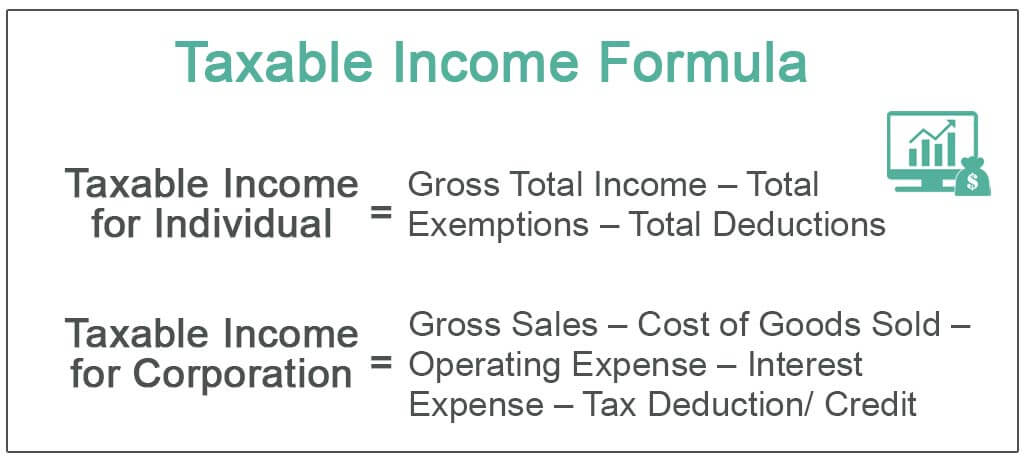

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

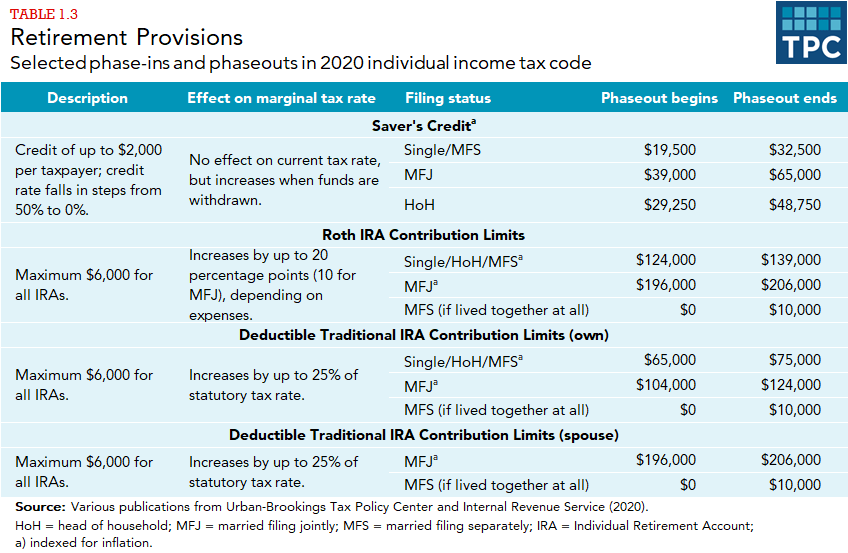

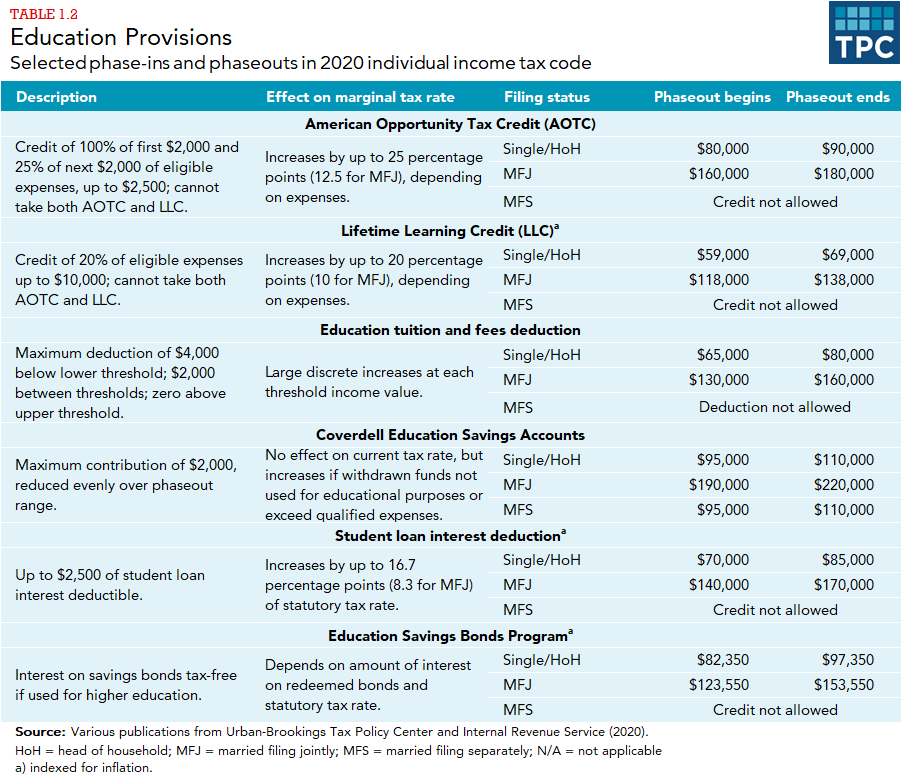

How Do Phaseouts Of Tax Provisions Affect Taxpayers Tax Policy Center

What Is The Standard Deduction Tax Policy Center

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

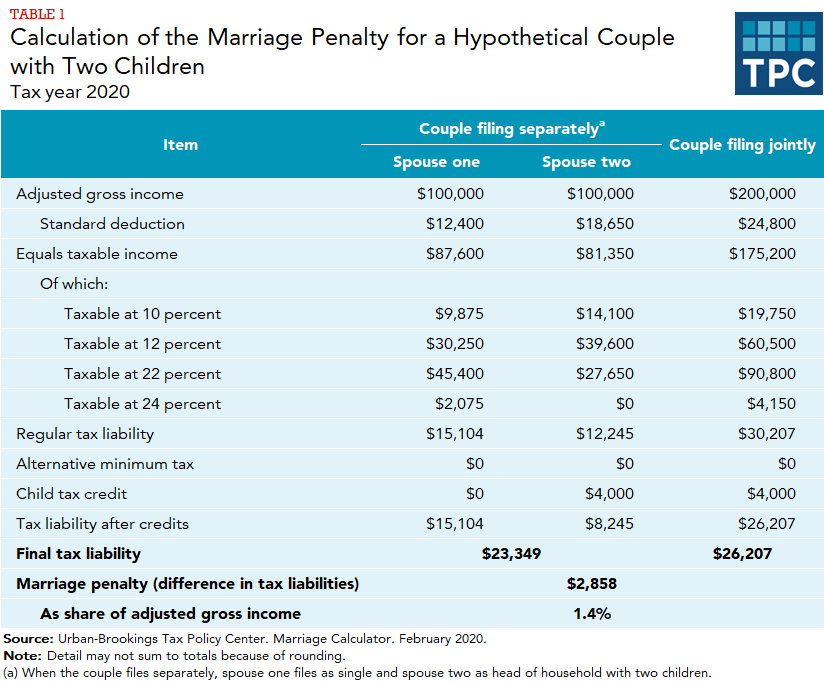

What Are Marriage Penalties And Bonuses Tax Policy Center

Tax Withholding For Pensions And Social Security Sensible Money

How Do Phaseouts Of Tax Provisions Affect Taxpayers Tax Policy Center

Annuity Exclusion Ratio What It Is And How It Works